> [!meta]- Document Info

> **Author**: [[readwise.io]]

> **Full Title**: 2024 SaaS Benchmarks Report by High Alpha

> **Category**: #articles

> **Tags**: #entrepreneurship #go-to-market #management #research #saas #startups #strategy #tech

>

>

> **Source**: [Original URL](https://readwise.io/reader/document_raw_content/241245044)

## 📄 Full Document

→ [[2024 SaaS Benchmarks Report by High Alpha]]

## 🔦 Highlights & Commentary

- balancing growth with efficiency ([View Highlight](https://read.readwise.io/read/01jda4pe6b2pdqzyn8654f0vgv))

- Note: Growth at all costs -> PEG -> ?

- Companies with less than $1M ARR saw their median year-over-year growth rates rebound to 100%, up from 90% in last year’s survey. While larger companies in the survey saw continued declines in their year-over-year growth rates, companies with top quartile net dollar retention showed improvement over 2023. ([View Highlight](https://read.readwise.io/read/01jda4x4b0j7t83bk1nhptvqwa))

- Note: Incumbents losing ground to AI-native entrants

- AI-native companies are growing more efficiently than past early stage companies ([View Highlight](https://read.readwise.io/read/01jda4rjpg5gryjtexvmwabzct))

- nearly one-third of all dollars invested in 2024 through August into AI ([View Highlight](https://read.readwise.io/read/01jda4w5a5agyasndhh14chbkw))

- Note: new investment paradigm

- helping you get work done to getting work done for you. ([View Highlight](https://read.readwise.io/read/01jda4ryc0pg7ehxd4t346x5jp))

- Note: Shifts in P&P lag this -> pay for outcomes/success

- Net Revenue Retention ([View Highlight](https://read.readwise.io/read/01jda4yq4fwd9w3ngc0w2y1a54))

- Note: This doesn't work in a pure pay-per outcome/success model. More challenging in hybrid models as well (subscription + consumption) with an element of modeled forecasting.

-  ([View Highlight](https://read.readwise.io/read/01jda55pta5eage5tjvyc3c9kj))

- Note: Up to 50% on S&M

-  ([View Highlight](https://read.readwise.io/read/01jda549dz5zfcat7pxrqgq95k))

- Note: 90 - 95% GRR

100 - 105% NRR

-  ([View Highlight](https://read.readwise.io/read/01jda5cerb1z13hfa86v55jg1x))

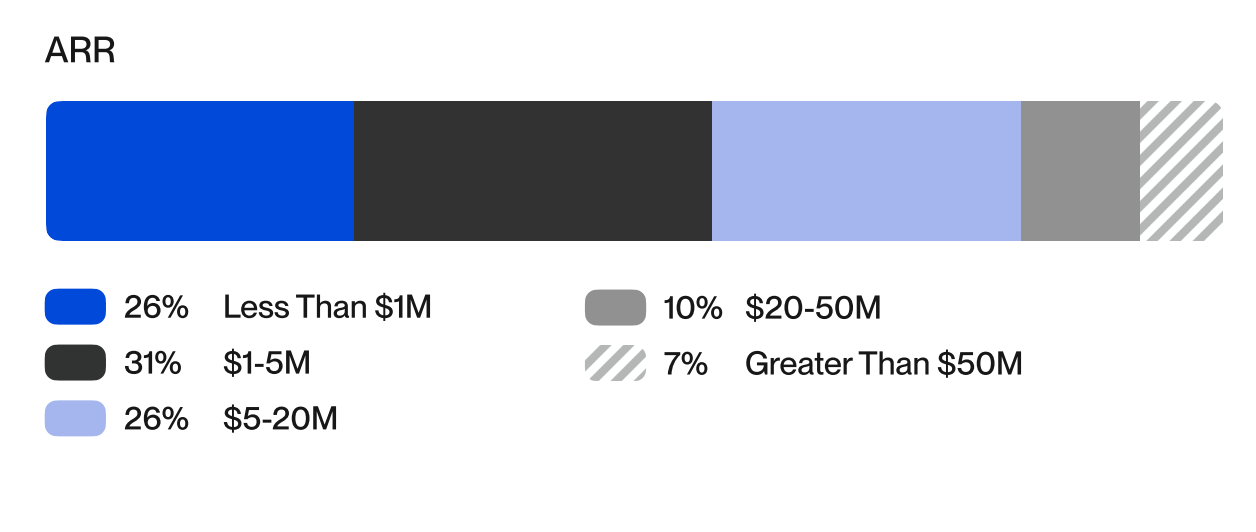

- Note: heavy <1-20 representation, ~80%

- , public SaaS company growth and retention rates have stabilized, albeit at a lower level than in prior years. ([View Highlight](https://read.readwise.io/read/01jda5gparr2f235eecw2w5bs9))

-  ([View Highlight](https://read.readwise.io/read/01jda5fswrmewxhs0r2cpwq66q))

- Note: broad compression + shift to PEG

- Venture Capital Deal Activity Hovering Near Pre-Pandemic Levels ([View Highlight](https://read.readwise.io/read/01jda5j7f2e8p9dw5zc34xmndx))

- Note: VC activity + retention rates stabilizing at or near pre-pandemic levels--how much of 2021+ is inflated/correction?

- The market still values growth over efficiency, so continued improvement in growth rates is critical for funding. ([View Highlight](https://read.readwise.io/read/01jda5p0vxsh7yfgd3sd608m14))

-  ([View Highlight](https://read.readwise.io/read/01jda5mmxw47fqzsdnq5j1g1fa))

- Note: 5-20M double digit YoY is the meta target

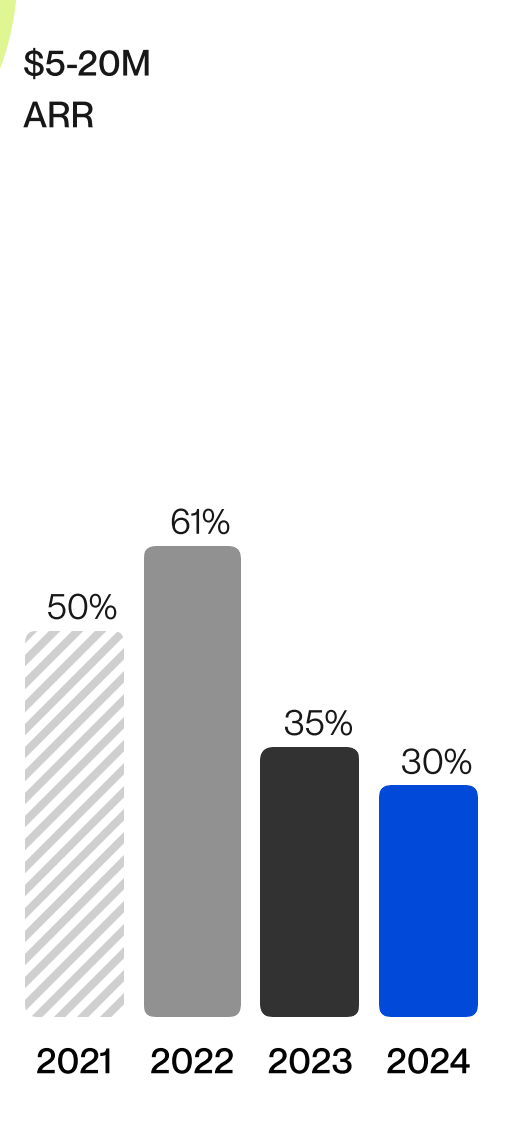

- Top quartile revenue growth for companies with over $50M in ARR is now less than half of what it was in 2021 and 2022. ([View Highlight](https://read.readwise.io/read/01jda5s1te461e6y4fmb5hb5hq))

- Note: Logistic growth curves

dN/dT = Vmax (1-N/K)N where N = market share and K = market saturation

- AI-Native & Vertical SaaS ([View Highlight](https://read.readwise.io/read/01jda69t3bmehk78yr487zreap))

- Note: a case against platforming, we'll see this shift again though. too many tools.

- revenue expansion opportunities are driving their AI strategy. ([View Highlight](https://read.readwise.io/read/01jda6cmwxj4hjr0vqkh8y6rca))

- Note: AI as revenue lever.

"AI for X" era should be just about saturated/no longer novel. Real P&P requirements imminent.

Usage/outcome based commercial models change the consumption modality and the value roadmap. Pre SaaS you buy the software, traditional SaaS you buy access, post AI you by the agent. (CDs -> spotify -> AI DJ)

- Result or Output Driven ([View Highlight](https://read.readwise.io/read/01jda6btvkx0rpvftdjy2n6ndp))

- Note: starting to accelerate here, will blow up saas metrics

- Many Large SaaS Companies Are Shifting to Output Driven Pricing ([View Highlight](https://read.readwise.io/read/01jda6nq0mcnz69df906vthwqq))

- Note: Final death knell of predictable revenue here. You can't use straightforard benchmarks "predict" revenue performance, ergo can't raise/lend/comp on those targets either. We'll see a big shift toward one-time/service eseque billings. Forecasting and valuations will have to be modeled.

-  ([View Highlight](https://read.readwise.io/read/01jda6phre33dcrv65p3w7s66z))

- Note: Median $10MARR is spending $3.5M on S&M, from 35% YoY growth, ~66FTEs

- companies are much more cautious with burn and are finding ways to sell and serve customers with fewer resources. ([View Highlight](https://read.readwise.io/read/01jda6zhmezr5akccwhfjkwqcy))

- Note: PEG shift largely fueled by shrinking/compressing gtm teams

- Despite the Increases, Employee Counts Are Still Lower Than 2022 Levels ([View Highlight](https://read.readwise.io/read/01jda71bfr9r8fe9ymk8n0f7bb))

- Note: Room for growth, but will lag overall performance in sustainable growth markets

-  ([View Highlight](https://read.readwise.io/read/01jda76p34zyxnwv6tc4thd78e))

- Note: Median 22, ~3.5x mutliple

- 1-500 Employees ([View Highlight](https://read.readwise.io/read/01jda7aa366f92nj0mfzzd1xh6))

- Note: Workflow tools vs. FTE

-  ([View Highlight](https://read.readwise.io/read/01jda7bwgvff7jnpzckqbt8wfr))

- Note: big range with big implications for lifecycle

- NRR ([View Highlight](https://read.readwise.io/read/01jda7f4d05dpkvw970ekvm0sc))

- ?t=1732288995150 ([View Highlight](https://read.readwise.io/read/01jda7gjg86284mdtb5f0j880a))

- Note: Biggest bang for marketing investment still in maximizing reach, but need enough stability in CAC/GRR for investments to impact revenue (~4-6Qs)

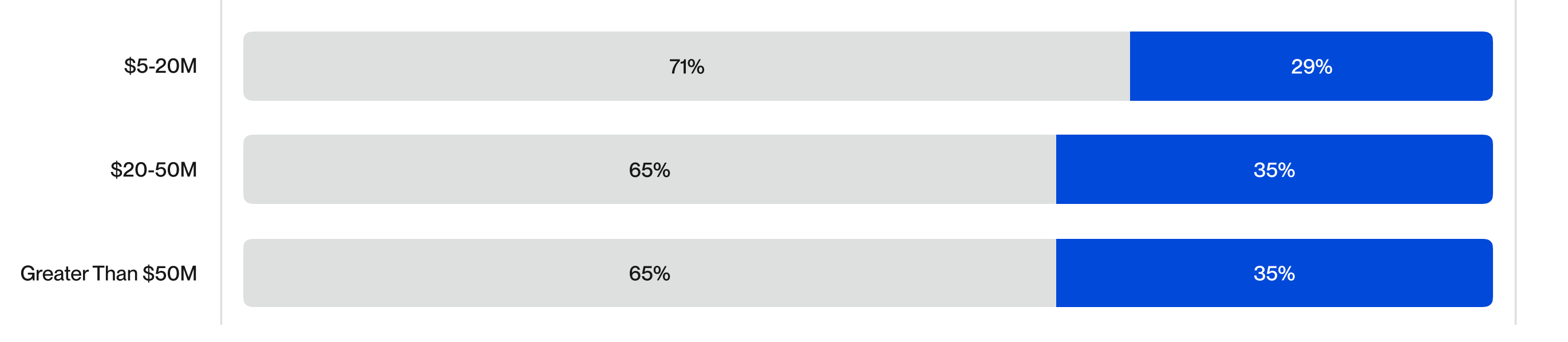

- Companies With ACVs of $25k to $50k Are Growing Fastest ([View Highlight](https://read.readwise.io/read/01jda7n5yzh57d0zavcya17512))

- Note: Sweet spot here in velocity/volume

- of the 37% of companies that don’t attach any paid services to their deals, nearly half have ACVs greater than $25K. ([View Highlight](https://read.readwise.io/read/01jda7pda1he0epjard0c59wnh))

- Note: Services for onboarding/adoption/success in sales-led orgs lead PLG trends. New consumption models will make this even more critical, blurring the lines between AE/CSM.

- Gross margin is an often overlooked key SaaS metric, but is critically important to a company’s financial health and scalability. ([View Highlight](https://read.readwise.io/read/01jda7t0tc06nx6v074cj5pf95))

- Note: "More than one way to skin a cat" as they say

-  ([View Highlight](https://read.readwise.io/read/01jda8d7nkpvnw1sagfrmsedse))

- Note: Median org is 11 Sales/5 Marketing--that's a reasonable split

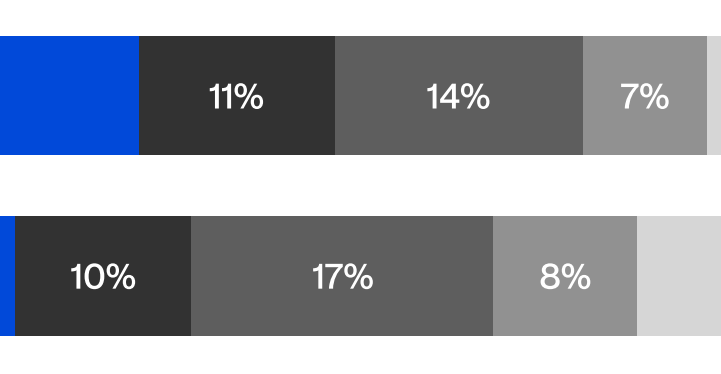

- Finance is the Most Popular Function Being Supported By Fractional Executives Across All ARR Bands ([View Highlight](https://read.readwise.io/read/01jda8g9bms9957c16p38rptbb))

- $20-50M ([View Highlight](https://read.readwise.io/read/01jda8jbdkbz7w7745zcesge40))

- Note: 20-50M fractional marketing at 30%?! Hypothesis: growth experience +20M much more rare/critical.

- arge tech companies are increasingly mandating return to office policies. ([View Highlight](https://read.readwise.io/read/01jda8pbqhr6pcedtvt6jp8jjt))

- Note: selection bias?

- GTM continues to weigh on founders, and has increased every year since 2021. Cash burn concerns have decreased, moving from 32% in 2023 to 28% in 2024. ([View Highlight](https://read.readwise.io/read/01jda8r94akd2mx1pczt6nfdm9))

- Note: GAAC -> PEG = cut growth captial and FTE but slow growth

PEG -> sustainable growth = finding growth rates with "efficient" teams